Growing up in Indian Households, we have all probably heard this, “Koi bhi Karza Accha Nahi Hota”. For our parents and even older generations, any kind of debt was a strict NO.

Fast forward to today, EMIs are the norm – phones, laptops, household equipment, vacations, and even weddings. Loans and EMIs have become so common and have crept in our finances but often in a wrong way.

Before we label all kinds of debt as evil or embrace every EMI, let’s get a clear idea of Good Debt vs Bad Debt – and how to decide what’s right for you.

Why this Conservation matters

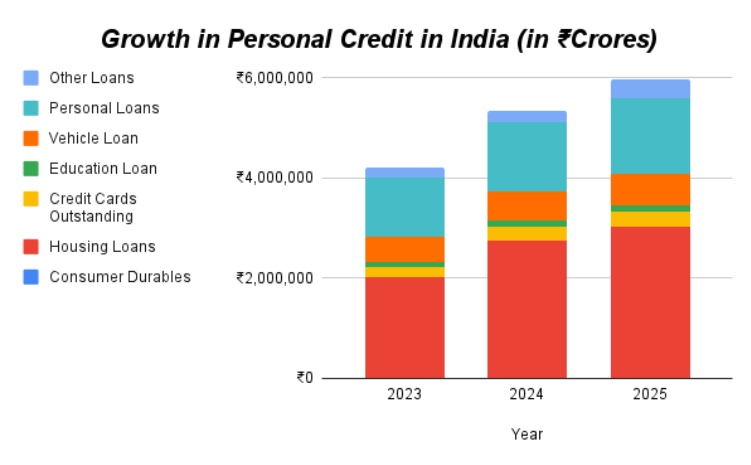

India’s appetite for credit has surged in the recent years. Personal Credits in India i.e. Loan taken for personal purposes like Housing, Education, Vehicle, etc. has surged from ₹42.20 Lakh Crores in Apr 2023 to ₹59.81 Lakh Crores in Apr 2025. The chart below shows the growth in Personal Credit by sections.

Source: RBI, EduFund Internal Research

From the chart, it is clear that there has been a substantial increase in borrowings by Indian Households. Hence, it becomes more important than ever to understand if debt is good or bad.

Debt is a double-edged sword. Used right, it can be the wings that help you reach your goals faster. Used wrong, it can handcuff your cashflow, delay investments, and keep you financially stuck.

What is Bad Debt?

Bad Debt usually funds things that:

- Don’t grow in value or generate income i.e. depreciating assets or consumable items.

- Lose relevance quickly – impulse purchases, luxury items that you don’t need, or a buy because, “Sale Tha, Le Liya!”

- Traps you in High Interest and/or EMI – Credit Card Debt, High Loan amounts that translate into High EMIs.

Examples of Bad Debt: Upgrading a phone that you didn’t need, a lavish vacation on EMI, taking a car loan that stretches your budget.

What counts as Good Debt?

Good Debt is borrowing that builds your net worth or boosts your future earning power.

- Education Loan that meaningfully increases employability and income potential.

- Business Loan with a clear business plan and positive expected return.

- Home Loan for a house that you can comfortably afford in a stable and stable location.

- Skill Building or Certifications tied to career progression.

Marking the Difference using an Analogy

Let’s understand how you can differentiate Good Debt and Bad Debt with an Analogy.

Avinash is planning to buy a Car by funding 20% from his own pocket and remaining 80% with a Car Loan. Car is a depreciating asset and the value of it decreases the moment the car leaves the showroom.

Price of the Car:– ₹10 Lakh.

Loan Borrowed:– ₹8 Lakhs.

Total Cost including Interest:– ₹12.32 Lakhs

Car Value after 5 Years:– ₹4 – ₹5 Lakhs

So here, Avinash is funding a depreciating asset with a loan that will end up him costing more than the original price of the car.

Ravinder wants to purchase a property for which he is considering taking a home loan on it. He decides to make a down payment of 30% of the property while financing 70% with the home loan. He is also planning to rent out the property for a few years before selling it. Here, the property has the potential to appreciate as well as generate cashflows in case it is let out.

Price of the Property:– ₹50 Lakh.

Loan Borrowed:– ₹35 Lakhs (10 Years @ 8.5%)

Total Cost including Interest:– ₹67.1 Lakhs

Total Net Rental Income (2%-3% yield):- ₹10-₹15 Lakhs

Property Value after 10 Years:– ₹74 Lakhs (4% CAGR)

Ravinder used debt for funding an appreciating asset that helped him generate regular cashflow as well as gains on the same. Also, this home loan will help him gain tax benefits, potentially increasing his after-tax income.

The Grey Zone – Where Mistakes Happen

But here’s the thing: Some loans aren’t inherently “Good” or “Bad”. A Home Loan can be a great wealth builder; but if the EMI eats larger portion of your budget, it quickly becomes Bad Debt in practice.

A few examples on this:

- Home Loan: Good Debt only if EMIs are affordable, location is sensible and lets you invest alongside. Overshoot your budget and the EMIs can crowd out your savings, delay other important goals, and it will end up turning into a long and painful home loan.

- Car Loan: Can be reasonable if there’s actually a need for vehicle and the EMI is modest. Becomes Bad Debt when it’s purely aspirational and strains cash flow.

- Education Loan: Generally Good Debt, but course, college, and expected salary matters. An expensive program with poor outcome can fail your math.

The Checklist: Identify Good Debt & Bad Debt

Ask these things before signing or confirming any loan application.

1. What is this debt funding?

Assets or Skills that appreciates or earns (business, property, education) = Good Debt

Consumption or Lifestyle (vacation, luxury, unnecessary upgrades) = Bad Debt

2. Will it improve my finances later?

Higher expected income, rent/savings, or business cashflows? Good

No clear future benefit? Bad

3. Is this an affordable loan FOR ME?

Keep total loan EMIs ≤ 30–40% of monthly take-home.

Maintain 6 months of expenses including EMI expenses as Emergency Fund

Stress test for low hikes or income drops. If numbers stress up, it is not good for you.

4. Will there be any investment room?

If EMIs leave no space for regular investing, even a Good Debt on paper may be bad for your plan.

5. Am I okay with the Tenure and the Total Cost of the Loan?

Lower Rate + Flexible Prepayment + Reasonable Tenure = Good Debt

High Interest + High Prepayment Charges + Long Tenure = Avoid

6. Is there any Plan B?

What if things don’t work out as I planned? Is there a clear exit or prepayment strategy? Am I insured enough so that the debt won’t pose a problem for my dependants? If you don’t have answers for this, rethink!

Putting it Together

Your parents weren’t entirely wrong when they said the lines. Unchecked borrowing is definitely dangerous and is a big No! But in a modern economy where borrowing is easily accessible, smartly chosen Debt can accelerate your goals. The magic is discipline and fit.

Borrow for building assets and skills, not for impulses. Keep EMIs light enough so that you can consistently continue investing.

Debt is neither a villain nor a hero. It can be your tool. Use it to build, and not to brag. If you are unsure if your loan qualifies as Good Debt or Bad Debt for your situation, run it through the checklist that we provided above, and you’ll rarely go wrong.

People Also Ask

What is the difference between Good Debt and Bad Debt?

Not all debt are the same. Good Debt helps you build assets or increase your potential future earnings / cashflows. Bad Debt funds depreciating assets or consumable items.

How do Rich use Debt to get richer?

Rich use debt to enhance their financial position and create long term wealth by investing in appreciating assets such as real-estate or highly profitable businesses.

Why do Billionaires like Debt?

Debt by default is not bad. The difference depends on how you use Debt. As a tool or as a showpiece. Billionaires like Debt because it enables them to build their networth by buying appreciating assets.

Disclaimer: The data in this presentation are meant for general reading purpose only and are not meant to serve as a professional guide/investment advice for the readers. This presentation has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been suggested or offered based upon the information provided herein, due care has been taken to endeavor that the facts are accurate and reasonable as on date. The information placed on the presentation is for informational purposes only and does not constitute as an offer to sell or buy a security. The Company reserves the right to make modifications and alterations to the content available on the presentation. Readers are advised to seek independent professional advice and arrive at an informed investment decision before making any investment. The EduFund platform & the website is owned, operated and maintained by Helena Edtech Private Limited, a company incorporated under the laws of India. An affiliate of the Company, i.e. Edubillions Tech Private Limited is registered with AMFI as mutual fund distributor bearing the registration number ARN258733. Investment in securities market are subject to market risks, read all the related documents carefully before investing. The valuation of securities may increase or decrease depending on the factors affecting the securities market.

About the author

Niraj Satnalika

Head Of Research,EduFund

Dr. Niraj is a finance professional with 12+ years of experience and is part of the founding team at EduFund. He’s worked with Goldman Sachs, CRISIL and Sakal Media in roles spanning investment management, research and leadership. With a PhD in Finance from IIT Bombay, he brings deep expertise in valuation, governance and education planning. When he’s not teaching or writing, you’ll find him cooking or going on long drives.