What if we told you that you could be a crorepati without going to KBC or without winning a lottery? Would you want to follow that mantra and build a huge corpus for yourself?

The Mantra is called *drum roll* the 15 x 15 x 15 rule of investing!

It means that, if one follows a diligent financial discipline of investing Rs 15,000 for 15 years in a mutual fund that offers returns of 15% – one would be building a huge corpus that would be greater than Rs 1 Cr.

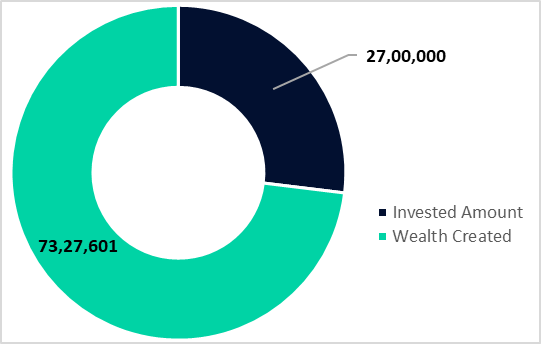

Upon investing Rs 27 lakhs, one creates a wealth of over Rs 73 lakhs!

| SIP – 15 x 15 x 15 | |

| Amount | 15000 |

| Expected Return | 15% |

| Number of years | 15 |

| At the end of the time period – Maturity | |

| Invested Amount | 27,00,000 |

| Wealth Created | 73,27,601 |

| Final Amount | 1,00,27,601 |

If one continues this financial discipline and continues to invest for another 10 years the corpus would build to Rs 4.86 Cr i.e., 4X times in another 10 years.

If you want to maintain this for another 15 years i.e., the entire period of investing would be 30 years – the corpus would be over Rs 10.38 Cr which is 10X times what one would have obtained for being invested for 15 years.

Compounding has a magical effect on our investments by growing our small contributions into a large sum. Hence, it is always advisable to start the magic early – because “Kal kare so aaj kar aur Aaj kare so ab” applies even to your portfolio of investments.

Consider that you would like your child to study in a reputed Ivy league school or a grand college in the States (US). The current tuition and fee for a Public 4-year program are $10,560, which is Rs 7.65 lakhs after the $/Rs conversion rate (1 $ = Rs 72.59). However, this is for a resident of the state.

For Indian students or out-of-state students, the fees would be $23,890/year – for 4 years it would be $95,560 which is Rs 69 lakhs. The tuition and fees have increased by 16% over the period of 2011-21 (inflation-adjusted). This implies that after 20 years the fees would rocket to over Rs 1 Cr.

Hence, one would have to take this factor of “educational inflation” into consideration when one is saving for their little one’s education. Similar to all investments, it is always better to start as early as possible to reap the benefits of compounding.

If your child is to pursue his/her higher education after 15 years, you could follow the 15-cube mantra (15*15*15) to fund the dreams of your little one.

| Education Expenses Today | 70,00,000 |

| Education Inflation (over 10 years) | 16% |

| Number of years | 20 |

| Expected Education expenses (future) | 94,19,200 |

| Monthly saving required | 6,697 |

| Expected return rate | 15% |

| Time Period | 20 |

There could be cases where you have a higher time frame for your child.

For example: If your child is 2 years old, and would fly off to pursue his or her education after 20 years, the amount that you should be saving to fund his/her education effortlessly would be as shown in the table.

Hence as a parent, you would have to save Rs 7000/month to fund your child’s education. The easy way to do this is by downloading the EduFund app and getting started on your investment journey to fulfill your child’s dreams.

FAQs

What is the 15 * 15 * 15 Rule in Mutual Funds?

It means that, if one follows a diligent financial discipline of investing Rs 15,000 for 15 years in a mutual fund that offers returns of 15% – one would be building a huge corpus that would be greater than Rs 1 Cr. Upon investing Rs 27 lakhs, one creates a wealth of over Rs 73 lakhs!

What is the average return in SIP for 15 years?

SIPs in mutual funds can generate an average return of 15 to 18% over the duration of 15 years. However, this return can change according to market changes.

Which SIP gives the highest return in 5 years?

Axis Bluechip Fund Monthly SIP Plan

ICICI Prudential Bluechip Fund

SBI Bluechip Fund

Mirae Asset Large Cap Fund

SBI Multicap Fund

Is mutual funds taxable after 10 years?

Yes, you need to pay the applicable taxes only when you redeem the units or sell the scheme. However, your total income for the financial year in question includes your dividend income from mutual fund schemes.