Many investors with a lump sum – from a bonus, property sale, or inheritance often hesitate to invest it all at once due to market volatility, leading to capital sitting idle in low-yield accounts. A Systematic Transfer Plan (STP) offers a disciplined, methodical approach to gradually deploy this sum, mitigating risk and fostering wealth.

STP leverages market fluctuations by spreading investments over time, averaging purchase costs and building a more resilient portfolio. In this article, we explore STP and how you can use it to invest your Lump Sum gradually in the investments of your choice.

Quick Summary: Using STP to De-risk your investments

- What: Move fixed amount from a liquid/ultra-short debt fund to equity / long term debt at regular intervals.

- Why: De-risk entry with rupee-cost averaging; cash earns in debt while you wait; high liquidity.

- When: Bonus, inheritance, property sale, or other large inflow.

- How: Park lump sum; set weekly/monthly STP (e.g., ₹50k x 52 weeks).

- Tax note: Debt fund gains taxed at slab rates (post Apr 1, 2023); loss set-off/carry-forward allowed; FDs tax interest yearly. Caution: Market-linked, not guaranteed; check STP rules, exit loads, minimums.

What is STP? Your Systematic Path to Growth

A Systematic Transfer Plan (STP) lets you transfer a fixed amount from one mutual fund (your source fund) to another (your target fund) at regular intervals. Usually, you begin by parking your lump sum in a low-risk debt fund (like a liquid or ultra-short-term fund), and then slowly shift it into an equity or hybrid fund – all within the same AMC.

This way, your capital earns modest returns while waiting and gets deployed into equities gradually, reducing timing risk.

How does STP work? Let’s do a practical case study!

Imagine you’re sitting on a ₹50 lakh lump sum after a property sale. You don’t want to invest it all in equities at once because the market feels like a mood swing waiting to happen. Your options:

| Investment | Annual Returns | Reality Check |

| Savings Account | 3% | Doesn’t beat inflation |

| Smart Savings (Sweep-In FDs) | 4 – 5% | Slightly better, still doesn’t beat inflation |

| Traditional FDs | 6 – 7% | Locks in capital, low liquidity |

Now, contrast that with this plan:

1. Park your money in a liquid or short-term debt fund.

2. Set up an STP to regularly transfer, say, ₹50,000 every month into an equity fund.

Your money isn’t just waiting but it’s earning!

Here are the average returns of popular liquid debt fund sub-categories:

| Debt Fund Type | 1 Yr Return | 3 Yr Return |

| Short Duration | 8.61% | 7.87% |

| Floater Funds | 8.42% | 8.03% |

| Liquid | 6.95% | 7.01% |

| Overnight | 6.19% | 6.44% |

Source: ValueResearch. Data as on 28 Aug 2025

As you can see even the most conservative options like the Liquid Funds comfortably beat a savings account. Why let your money sleep when it can grow at a decent rate before entering the equity arena?

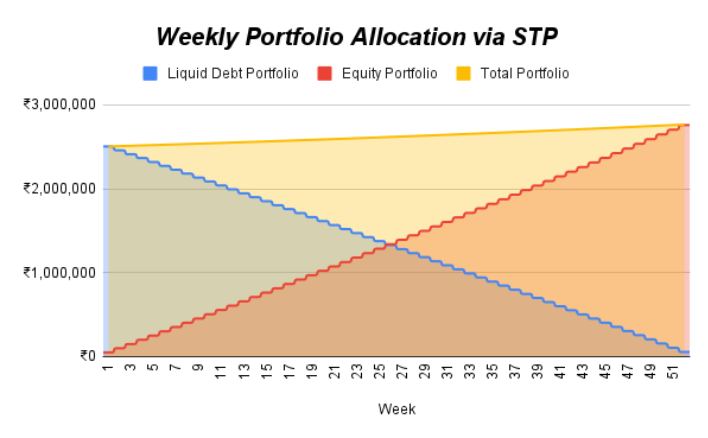

Let us take an illustration to understand this. Let’s say you have ₹25 Lakhs Lump Sum available with you that you are looking to invest in equity. You don’t want to take risk and invest all of it at once into an equity mutual fund. STP here becomes a valuable option for you, offering you the benefit of investing your money over a period of time regularly.

This reduces the potential risk of locking in a higher price and allows you to invest across the market cycle. For a ₹25 Lakh amount spread over 52 weeks, a STP of ₹50,000 is made into the equity fund from the liquid fund. Here’s how the portfolio would gradually shift from Debt to Equity.

Source: EduFund Internal Research, Value Research

Notice how the allocations happen from liquid debt fund to equity fund regularly over the weeks while the remaining debt portfolio keeps growing steadily.

Why STP is a win-win game?

No Market Timing Needed: Spreads out risk over time with rupee cost averaging.

Better than Idle Funds: Debt fund returns often outshine savings or even FDs.

High Liquidity: Most debt funds offer easy redemption, unlike fixed deposits.

Tax Benefits: With FDs, interest gets taxed every single year (even if you haven’t withdrawn).

For debt funds, the old indexation benefit is now gone (for investments after April 1, 2023), but they still allow loss set-off and carry forward.

Final Takeaway: Let Your Lump Sum Work Smart, Not Just Hard

A lump sum doesn’t have to be a burden of decision-making or a victim of market timing fears. With an STP, you gain control, consistency, and compounding – the “holy grail” of long-term wealth creation.

Rather than parking your money in low-yield options or gambling it all in one market entry, STP offers a steady glide path from safety to growth. It helps you ride market volatility like a seasoned investor while ensuring your capital is never sitting idle.

Even if you’re not keen on equity exposure right now – no pressure! You can still park your lump sum in a Liquid or Ultra Short Term Debt Fund, which often delivers returns far superior to a savings account or FD, along with high liquidity and better tax treatment.

Think of it as giving your money a cushioned seat while it stretches and earns.

In the world of investing, patience pays but strategy pays more. STP is that strategy!

So, next time life surprises you with a lump sum, don’t just bank it – Plan it, Park it, Transfer it! Let your money take the systematic route to prosperity.

People Also Ask

1. Is STP better than Lump Sum?

STP is often considered a better option than Lump Sum for those who want to mitigate the risk of investing all their money at once.

2. Which is better STP or SIP?

Both, STP and SIP offer a different usecase and are not substitutes of each other. Prefer SIP if you have a monthly investible surplus. Prefer STP if you have a lump sum amount and you want to invest it in the market gradually at a regular frequency.

3. Is STP in Mutual Fund taxable?

Yes. Switching from a Liquid Fund to an Equity Fund or from any other fund to another fund will trigger STCG or LTCG tax, depending on the investment age. It is taxable just like any other transaction in mutual funds even if it is from the same AMC.

Disclaimer: The data in this presentation are meant for general reading purpose only and are not meant to serve as a professional guide/investment advice for the readers. This presentation has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been suggested or offered based upon the information provided herein, due care has been taken to endeavour that the facts are accurate and reasonable as on date. The information placed on the presentation is for informational purposes only and does not constitute as an offer to sell or buy a security. The Company reserves the right to make modifications and alterations to the content available on the presentation. Readers are advised to seek independent professional advice and arrive at an informed investment decision before making any investment. The EduFund platform & the website is owned, operated and maintained by Helena Edtech Private Limited, a company incorporated under the laws of India. An affiliate of the Company, i.e. Edubillions Tech Private Limited is registered with AMFI as mutual fund distributor bearing the registration number ARN258733. Investment in securities market are subject to market risks, read all the related documents carefully before investing. The valuation of securities may increase or decrease depending on the factors affecting the securities market.

About the author

Niraj Satnalika

Head Of Research,EduFund

Dr. Niraj is a finance professional with 12+ years of experience and is part of the founding team at EduFund. He’s worked with Goldman Sachs, CRISIL and Sakal Media in roles spanning investment management, research and leadership. With a PhD in Finance from IIT Bombay, he brings deep expertise in valuation, governance and education planning. When he’s not teaching or writing, you’ll find him cooking or going on long drives.