Remember the game of Chuppan Chupai (Hide & Seek) that you must have played as a child?

What was the strategy that you applied back then? Every teammate would hide in a different place so that the seeker is not able to find all of the players at once. In essence, Diversification is all about this when it comes to investing.

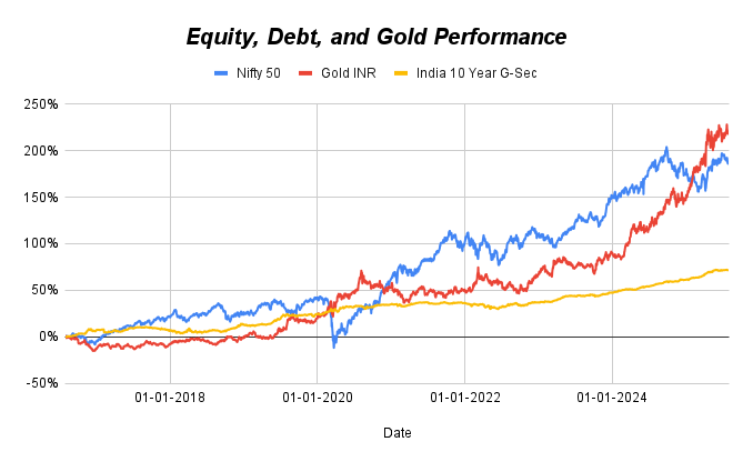

If the last few years has anything to teach us in investing, it’s this: Markets and Economy can throw Yorkers. From tariff wars to geopolitical tensions and other global uncertainties, equity and debt markets have felt the heat in the phases.

Even during the Covid-19 outbreak, while Indian equities sank sharply, gold and government bonds cushioned portfolios; exactly what diversification is supposed to do. Take a look at the graph that we have included below.

Quick Summary:

- Why diversify: Cushions shocks (pandemics, geopolitics), reduces drawdowns, and steadies compounding.

- What it is: Spread money across assets that don’t move together – equity, debt, gold, real estate – so one offsets another.

- How to do it:

- By asset class (equity for growth, debt for stability, gold as hedge, real estate for diversification)

- By horizon (short/medium/long-term goals)

- Across family members (PAN-wise tax efficiency)

- Across markets (add US/global to hedge INR depreciation)

- Myth buster: You may trail the top performer in any one year but may not gain better risk-adjusted returns over time.

- Set your mix: Know your risk profile, map goals to horizons, allocate, and rebalance periodically.

In 2020, while equities took on a roller coaster ride, Gold and Debt quietly sustained volatility helping the portfolios that would have held them.

And while the recent uncertainties have not been easy for equities, gold has been a front-runner. These examples proves that diversification is your answer to those deadly yorkers.

Source: EduFund Internal Research, Investing.in, Value Research.

We have chosen SBI Nifty 10 Year G-SEC ETF as a proxy for India 10 Year G-Sec Index

Portfolio Diversification: What it Means

Diversification simply means that you spread your investments across different assets that don’t move in the same direction all the time. Instead of investing your money in one asset or a single theme, you build a mix of it; so that when one of them struggles, there are others that can support it.

Remember the age old adage: Don’t put all of your eggs in one basket?

It’s like that but with your money!

How to Diversify your Portfolio?

Diversify across asset class

Blend Equity, Debt, Gold, Real Estate, and other alternatives to achieve portfolio diversification. The mix can depend on your risk appetite as well as your investment horizon.

Equity drives long term growth, Debt adds stability and income portion, Gold is a time proven hedge for crisis, and Real Estate can further provide diversification and income beyond these assets. The idea is not to pick a single winner. But a team of winners that play well across market cycles.

Diversify across Investment Horizons

All of your goals don’t arrive at the same date, correct? There are short term goals, medium term goals, and then there are long term goals.

Short Term goals deserve safer and liquid options. Medium term goals can see a blend of stability and growth. While Long Term goals can lean on equity for growth.

Matching your assets and investments to your horizon and goals ensures you stay on the right track without having to sell an asset at a wrong time.

Diversify across family members

Don’t invest through a single name. Using separate PAN of spouse / parents / children can improve overall tax efficiency by helping you utilise exemptions. This helps you increase your net returns. Ensure you document your investments well for lesser hassles.

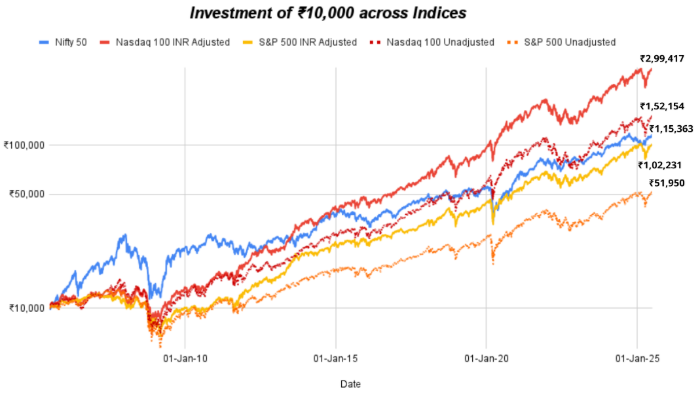

Diversify across markets

Gone are the times where you only had Indian equities to invest in. A small allocation to global equities – especially in the US adds breadth to your portfolio and also helps you hedge the currency depreciation.

The INR has historically depreciated against the US Dollar. Investments made in the US can help you in the sense that when you convert your USD investments back in INR, the depreciation works by your side to add your net returns. A graph below compares ₹10,000 invested in Nifty, Nasdaq, and S&P 500 with and without INR adjustment shows just how beneficial this can be for you.

Source: EduFund Internal Research, Investing.in

But won’t diversification lower my returns?

Pure equity portfolios help you top the charts during the bull market, for sure. A diversified portfolio might lag the best performer in any single year – but your aim should be to win consistently. Diversification helps you lower drawdowns, smoother compounding, and lesser panic decisions. This often translate to better risk adjusted returns which should matter the most for you.

How to figure out your Ideal Asset Mix?

Know your Risk Profile

The first step to find out how much portion you should have in each asset class is to understand your risk profile. How much volatility can you handle without losing your sleep or panicking at the bottom?

How much risk taking does your current financial situation allow you to? Take a risk profiling test or contact an investment advisor to better understand your risk profile.

Goal Based Investment Planning

It doesn’t matter if your risk profile is High and most of your goals are short term. Even then you won’t be able to invest your portfolio completely in Equity; because it can be risky for your goals. List down your goals, divide it into horizons to better understand where most of your goals fall. Allocate accordingly.

Closing Notes

The reason we keep talking about the benefits of Diversification isn’t just theory anymore; the recent years have proved its importance. During the chaos, diversification acts like shock absorbers helping you stay aligned with your long term plan.

Diversification doesn’t also mean that you own a bit of everything. It is about owning enough of the right things so that your portfolio survives on the bad days and thrives on the good ones.

Disclaimer: The data in this presentation are meant for general reading purpose only and are not meant to serve as a professional guide/investment advice for the readers. This presentation has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been suggested or offered based upon the information provided herein, due care has been taken to endeavor that the facts are accurate and reasonable as on date. The information placed on the presentation is for informational purposes only and does not constitute as an offer to sell or buy a security. The Company reserves the right to make modifications and alterations to the content available on the presentation. Readers are advised to seek independent professional advice and arrive at an informed investment decision before making any investment. The EduFund platform & the website is owned, operated and maintained by Helena Edtech Private Limited, a company incorporated under the laws of India. An affiliate of the Company, i.e. Edubillions Tech Private Limited is registered with AMFI as mutual fund distributor bearing the registration number ARN258733. Investment in securities market are subject to market risks, read all the related documents carefully before investing. The valuation of securities may increase or decrease depending on the factors affecting the securities market.

About the author

Niraj Satnalika

Head Of Research,EduFund

Dr. Niraj is a finance professional with 12+ years of experience and is part of the founding team at EduFund. He’s worked with Goldman Sachs, CRISIL and Sakal Media in roles spanning investment management, research and leadership. With a PhD in Finance from IIT Bombay, he brings deep expertise in valuation, governance and education planning. When he’s not teaching or writing, you’ll find him cooking or going on long drives.