Quick Summary 🏠📈:

- Pain point: Over 15 – 20 years, the home loan interest can equal or exceed the principal amount borrowed.

- The Hack? Start a monthly SIP = 1% of your annual EMI and run it for the same tenure as your loan.

- Illustration: ₹50L @ 8.5% (20 yrs) → interest ≈ ₹54.14L; SIP ₹5,200/m (1% rule) @ 13% assumed → corpus ≈ ₹59.56L; this effectively offsets interest.

- On a tight budget? Use a Top-Up SIP: start ~₹2,500/m, step up 10%/yr, still achieves the target corpus by year 20.

- Why it works: Long-tenure compounding builds a parallel corpus, easing the emotional & cashflow burden.

For most Indian couples, a home loan is the biggest financial commitment of their lives. The excitement of owning your dream home often comes with a long repayment tenure; 15-20 years and with interest burden.

What most home loan borrowers don’t realise is that over the long period, the home loan interest that they end up paying reaches almost equal to and sometimes even higher than the amount borrowed.

This can feel overwhelming and even disappointing knowing that you are paying substantial amount out of your pocket. What if there was a way to reduce your emotional burden?

There is – Start a Monthly SIP equal to 1% of your Annual EMI Amount to recover your Home Loan Interest. Sounds unbelievable? Today we break down this hack and show you how it is possible.

The Interest Trap

Let’s consider that you have taken a home loan of ₹50 Lakh at an interest rate of 8.5% p.a. for 20 years. The EMI for the same will be around ₹43,400. At the end of your home loan tenure, the total amount that you have repaid is ₹1.04 Crore and the interest amount that you ended up paying is ₹54.14 Lakhs.

This is even higher than your original home loan amount. Quite a shocker, right? But what if we told you that you can recover the entire amount by building an investment portfolio parallelly with a simple hack?

The 1% SIP Hack

Here’s the hack – Start investing 1% of your Annual SIP Amount as a monthly SIP in an Equity Mutual Fund. For example, the annual EMI amount in our earlier illustration would be ₹5,20,700; 1% of that would be ₹5200.

Invest the same via monthly SIP in an equity mutual fund for the same tenure as your home loan. Here is what will happen if you invest ₹5200 per month for 20 years, assuming 13% annual returns.

– Total Investment: – ₹12.48 Lakhs

– Total Portfolio Accumulated: – ₹59.56 Lakhs

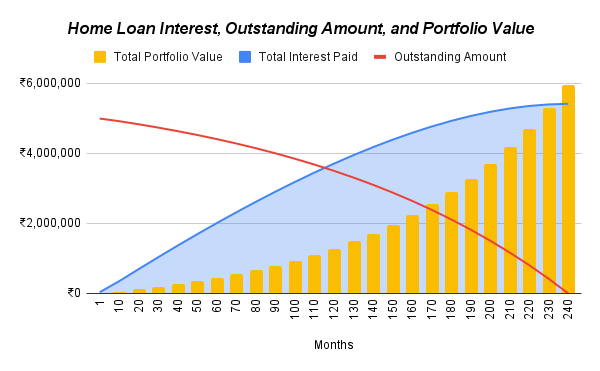

This is higher amount than your total interest amount and that too with a fractional of investment. Let us take a look at the working of this hack via a graph chart.

Source: EduFund Internal Research

As you can observe through this graph, the portfolio accumulation begins slowly, and over the years it swiftly catches up to the interest amount that you end up paying with your Home Loan. That’s the magic of the hack because of compounding.

Why this Hack makes sense for you

As you just understood, you don’t need a big amount to reap the rewards; just a small amount monthly equivalent to 1% of your Annual EMI is enough. This is because you are making time and compounding work for you.

As a result, over the years even a small amount like ₹5,000/month can end up growing to ₹50 Lakhs. Implementing this will offer you a peace of mind knowing that you are building a parallel corpus and will end up recovering your full interest amount by the time your home loan ends.

Till now, we thought of EMI as a one-way street – money going out and never coming back. With the help of this hack, you would be building a safety net that can be used for your other essential goals like Kid’s Education, Retirement Corpus, or even a Vacation.

What if your Budget is tight?

Paying a home loan EMI is already a stretch for many households. Adding a SIP on top of that might feel like too much. Here’s how you can tackle this – Consider starting a Top Up SIP instead of Normal SIP with your EMI. This will make your initial outgo even smaller and as your income increases in future, so will your contributions.

Continuing our earlier example, if you want to start a Top Up SIP to recover your Home Loan Interest, you need to start with just ₹2500 per month and increase the SIP amount by 10% every year to recover your interest amount fully at the end of 20 years. Now this will surely feel like a breather and much likely achievable target.

Final Words: Let your Discipline beat your Debt

In long-term investing, it is often the small and consistent actions that help you build something big. The 1% SIP Hack is no different. It doesn’t require you to time the market or find the best funds. All it requires is discipline and intent. If you have already committed to repay your Home Loan for the next 15-20 years, why not commit a small additional amount for yourselves?

People Also Ask

What is the 30/30/3 Rule for Home Loan?

This Home Loan Rules says – Spend on 30% of your monthly income on EMIs. Have 30% of the Home Value saved up to pay as a downpayment. And ensure that your budget does not increase 3 times your gross annual income.

Should I reduce my EMI or Tenure?

You should reduce the home loan tenure as reducing your EMI will only mean that the upfront payment gets lower while the interest that you end up paying won’t reduce much. But when you reduce your tenure, your EMI remains the same which means higher principal repayments and faster loan repayment; ultimately reducing your total interest outflow.

Can I pay extra EMI for home loan?

Yes, if you are able to arrange and make a payment for an extra EMI, you should definitely opt for extra EMI. This will directly go to repay principal amount reducing your outstanding loan amount and effectively reducing your total outflow. You should check if there are any prepayment charges before the same.

Disclaimer: The data in this presentation are meant for general reading purpose only and are not meant to serve as a professional guide/investment advice for the readers. This presentation has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been suggested or offered based upon the information provided herein, due care has been taken to endeavor that the facts are accurate and reasonable as on date. The information placed on the presentation is for informational purposes only and does not constitute as an offer to sell or buy a security. The Company reserves the right to make modifications and alterations to the content available on the presentation. Readers are advised to seek independent professional advice and arrive at an informed investment decision before making any investment. The EduFund platform & the website is owned, operated and maintained by Helena Edtech Private Limited, a company incorporated under the laws of India. An affiliate of the Company, i.e. Edubillions Tech Private Limited is registered with AMFI as mutual fund distributor bearing the registration number ARN258733. Investment in securities market are subject to market risks, read all the related documents carefully before investing. The valuation of securities may increase or decrease depending on the factors affecting the securities market.

About the author

Niraj Satnalika

Head Of Research,EduFund

Dr. Niraj is a finance professional with 12+ years of experience and is part of the founding team at EduFund. He’s worked with Goldman Sachs, CRISIL and Sakal Media in roles spanning investment management, research and leadership. With a PhD in Finance from IIT Bombay, he brings deep expertise in valuation, governance and education planning. When he’s not teaching or writing, you’ll find him cooking or going on long drives.